Selling Structured Settlements

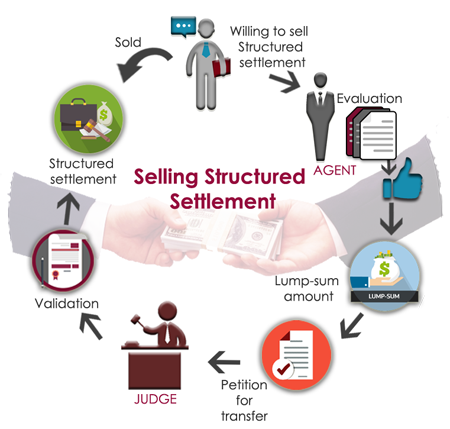

Selling a structured settlement or other scheduled payoffs was almost a societal decision during the recession. But it is not so anymore. Shortages of funds may still be experienced during the lifetime of an individual. Due to ongoing financial obligations, individuals may resolve to sell their structured settlement payments. Dire financial predicaments are forceful situations that can influence cashing in on a settlement. It is certainly a competent resolve to end all perennial financial vexes without thwarting life. Structured settlement annuities are contrived to provide regular tax-free remittances to casualties of personal injury over a prolonged period of time. Lump sum receipts may not be viable due to handling issues mostly related to bad judgments over bulk investments.

Monthly lawsuit disbursements in the United States amount to almost about $6 billion every year. Economic downturns attract a lot of selling of structured settlement payments due to financial deprivation.

{kind=link}

{kind=link}

Where for the structured settlement owner selling may be the only recourse available there are several limitations to the transaction. Lump sum payments are enticing to most sellers but encashing a settlement can result in surrender charges to the tune of about 10%. If an annuity is sold before the age of 59 ½ years the beneficiary from the sale is liable to federal taxes and penalties. The whole scheme of structured settlements has been fashioned to provide a tax-free lifelong income to the victim of injury. Overall, the legatee has to be wary of insurance companies with downgraded credit ratings. Of course, this is also assessed by the arbitrator during the final adjudication.